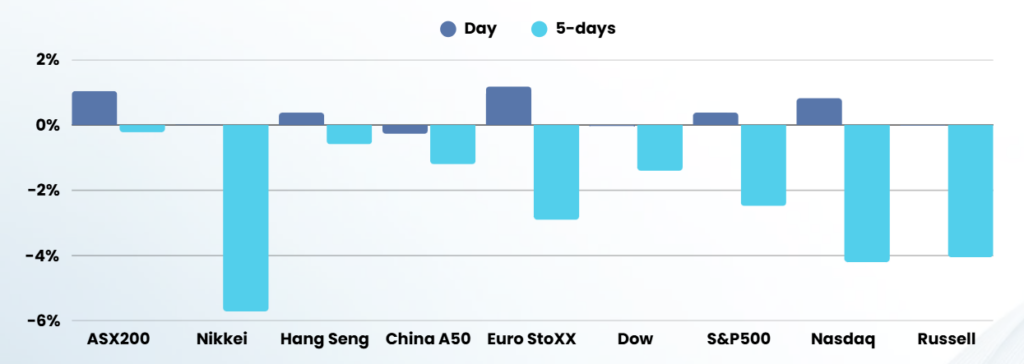

Overnight – Tech drags stocks higher into “Liberation Day”

Stocks recovered late in the session again, led by tech, despite cautious sentiment on risk assets ahead of President Donald Trump’s April 2 tariff announcements.

President Donald Trump is set to impose reciprocal tariffs on a broad range of trading partners on Apr. 2 that will go into effect immediately on Apr. 2, White House press secretary Karoline Leavitt said on Tuesday. “My understanding is that the tariff announcement will come tomorrow. They will be effective immediately,” Leavitt said.

Trump is considering a range of measures that could include a blanket tariff as high as 20%, a tired-tariff measure or a customized country by country basis. Trump is expected to announce the details of the administration’s reciprocal tariffs at 3:00 p.m. ET (7am AEDST)

This initiative, referred to as “Liberation Day,” will be followed by a 25% tariff on auto imports starting April 3. These measures are expected to significantly impact global trade dynamics and have raised concerns about their potential to contribute to recession risks. Goldman Sachs has increased the probability of a U.S. recession to 35%, up from a previous estimate of 20%, citing the anticipated rise in average tariff rates to 15%.

Signs of cooling in the labor market added to concerns about the economy ahead of of the all-important nonfarm payrolls report on Friday. The Job Openings and Labor Turnover Survey, or JOLTS report dipped to 7.568 million in February, down from an upwardly revised prior level of 7.762 million and just below the consensus of 7.69 million. Job openings are down 877,000 over the year, data from the Labor Department’s Bureau of Labor Statistics showed.

On the manufacturing front, meanwhile, ISM Manufacturing Index fell into contractionary in March, declining 1.3 points to 49.0, a four-month low.

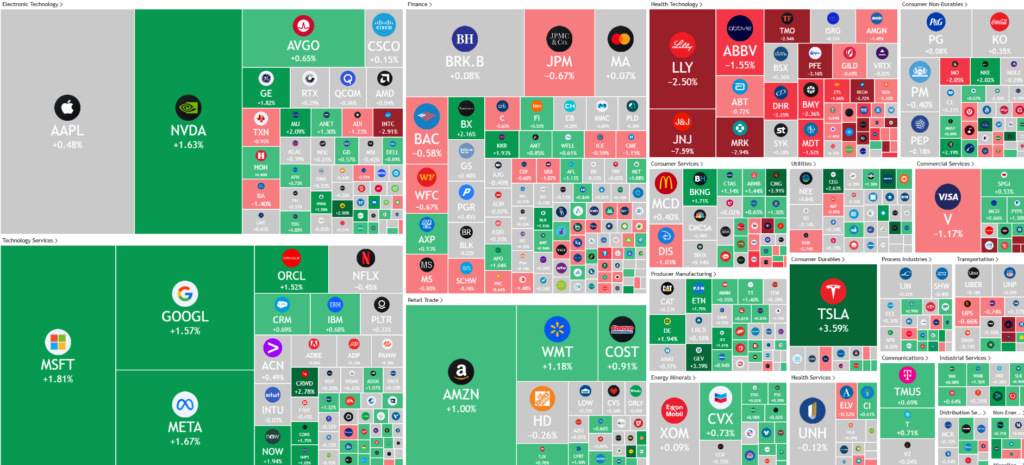

Company Specific

- Tesla was up 3%., led the broader move in tech higher just a day ahead of its Q1 update on deliveries. Ahead of the data, investors are bracing for weaker deliveries from the EV maker as rising competition and a softer demand weigh. Demand has been hurt by CEO Elon Musk’s political activity as part of the Trump administration. “While much of this softness is related to customers waiting for Model Y refreshes along with a lower cost new model set to be launched by the summer timeframe…the anti-Musk and brand issues are clearly at play and a major factor in this weak 1Q delivery number,” Wednesday said in a note.

- Johnson & Johnson stock fell 7.6% after a judge rejected the consumer healthcare giant’s $10 billion proposal to end tens of thousands of lawsuits alleging that its baby powder and other talc products cause ovarian cancer.

- PVH stock rose 18% after the luxury conglomerate, which owns brands such as Calvin Klein and Tommy Hilfiger, reported a fourth-quarter earnings and revenue beat.

ASX SPI 8001 (+0.35%)

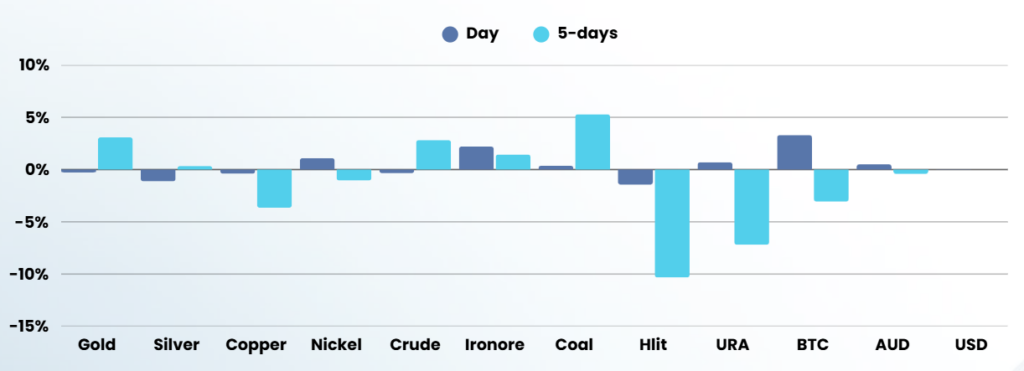

We should see another positive day for the ASX, led by the miners as iron ore jumped to 1 month highs.

Election promises and RBA analysis will be plentiful, while these might cause a short term reaction, over the long term its is very likely to be just noise.

Company Specific

- Paladin Energy has retracted its 2025 production guidance after unseasonably heavy rainfall significantly disrupted operations at its Namibia Langer Heinrich mine.

- Endeavour executive chairman Ari Mervis is undertaking a major review of the owner of Dan Murphy’s liquor stores and hundreds of pubs which could ultimately lead to the break-up of the hospitality company.

- IAG, Greensill Capital’s biggest insurer, is trying to delay a $7 billion trial over insurance claims, stating it needs more time to review more than one million documents as it opposes creditors’ calls to disclose reinsurance policies.