Skip to content

Skip to content

Last Night's Market Recap

Overnight – Solid retail sales dent rate cut hopes

Equities continued to drop as Treasury yields advanced, squeezing tech after stronger-than-expected economic data muddied investor expectations for a Federal Reserve March rate cut.

U.S. Treasury yields continued to climb higher, with the yield on the 10-year Treasury note rose further above 4% to hit highest level this year after U.S. retail sales rose 0.6% in the month of December, topping expectations for 0.4%. Signs of a stronger consumer, which makes up about two-thirds of economic growth, suggesting the economy remains in good share dented expectations for a rate cut as soon as March. The odds of a March rate cut fell to about 50% from 61%

Tesla fell more than 2% after slashing the price of its Model Y prices in Europe, triggering fresh concerns about margin pressures following several price cuts last year. The latest slump in the EV maker comes a day after Elon Musk said he would prefer to “build products outside of Tesla” unless the board raises his stake in the company to 25% from his current stake of 13%.

Apple fell for a 4th straight session as the ban on the sale of Apple Watch models with the blood oxygen feature in the U.S. will be reinstated on Thursday after The U.S. Court of Appeals for the Federal Circuit today denied Apple’s request to continue to allow imports of the watches amid a patent dispute with medical device maker Masimo

Energy stocks fell 1% as oil prices even as oil prices rebounded from session lows following disappointing growth data from China, the world’s second-largest crude consumer, raised concerns about future demand increases.

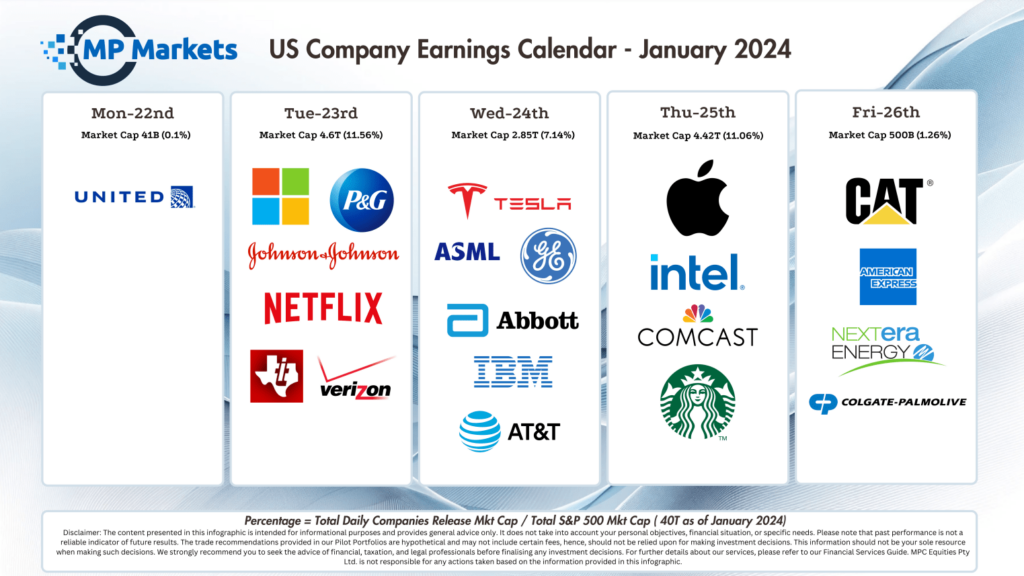

US Earnings

- Charles Schwab stock fell 1% after the financial services group reported a 22% dip in net profit in 2023, saying it dealt with “challenges” posed by a tighter interest rate environment.

- Interactive Brokers rose 2% after fourth-quarter revenue topped analyst estimates, though earnings fell short of expectations as net interest income fell in Q4.

S&P 500 - Heatmap

Commodities & FX

Bonds

The Day Ahead

ASX SPI 7333 (-0.20%)

We are likely to have a soft day on the ASX with the focus on domestic employment numbers at 1130. The recent trend of stronger than expected economic numbers in the US and AU is making Central banks job harder, as the market has falsely started expecting them to cut. Investors will be very disappointed expecting rate cuts in H1 this year, a risk to equity markets at near record highs

- Ampol expects its full year unaudited replacement cost operating profit (RCOP) earnings before interest tax to be slightly ahead of its record in 2022.

- According to the fuel refinery and retailer, its growth in earnings from non-refining divisions “offset a reduction in refinery earnings from the historically high levels in the prior year.”

- APM Human Services International has issued an aftermarket profit downgrade regarding its first half performance.

- The human services group’s preliminary and unaudited 1H24 results forecasts revenue of $1.14 billion, underlying earnings before interest and amortisation of $148 million, and underlying net profit after tax of $55 million.

- BHP and Yancoal are set to release production updates on Thursday.

Calendar

Economic