Skip to content

Skip to content

Last Night's Market Recap

Overnight – Fresh highs in bond yields squash earnings positivity

Equities fell overnight led by tech, as investor sentiment was soured by Nvidia-led weakness in chip stocks and a jump in Treasury yields following stronger retail sales data that boosted bets on a Fed rate hike by year end.

Treasury yields continued their surge higher, with the yield on the 2-year treasury rising to a 17-year high after better-than-expected retail sales pointed to ongoing economic strength, suggested the Fed still has more work to do.

Retail sales rose 0.7% last month, markedly beating economists’ forecast for a 0.3% rise. The retail sales control group – which has a larger impact on U.S. GDP – rose 0.6% well above expectations for a 0.1% rise. While a November rate hike remained low at 10%, the odds of a December hike jumped to 42% from 26% the prior week, according to Fed Rate Monitor Tool.

NVIDIA fell more than 5% to lead the broader chip sector lower following a Bloomberg report that the U.S. is restricting the sale of semiconductors that the chipmaker designed for the Chinese market. The tighter restrictions would now include Nvidia’s A800 and H800 chips, the lower performance GPUs, that Nvidia devised after the initial U.S. exports last October. The expanded curbs come as the U.S. aims to curb loopholes that allowed Chinese firms to evade export controls introduce last year by routing chip shipments through other nations.

Earnings Results

Bank of America reported quarterly results that topped Wall Street, sending its share more than 2% higher.

Goldman Sachs’ Q3 earnings, however, missed estimates amid losses from its real investment and Greensky fintech business. The bank suffered a $358 million write down on its real estate investment as the sector has come under pressure from a sharp surge in interest rates.

Johnson & Johnson upgraded its annual guidance on performance after reporting quarterly results that beat on the top and bottom lines, but the pharmaceutical company’s stock was 1% lower.

Lockheed Martin fell nearly 1% as the defense company’s third-quarter results topped analyst estimates, though concerns about the impact of delivery delays for its F-35 jets weighed.

S&P 500 - Heatmap

Commodities

Bonds

The Day Ahead

ASX SPI 7100 (+0.28%)

The positive results from the banks and the rally in Iron ore should keep the ASX relatively positive today with a raft of Chinese economic data to be released at 1pm AEDST. Rising yields were already in play in yesterdays session with Japanese bonds hitting fresh highs and the RBA minutes showing we narrowly missed another rate hike last month.

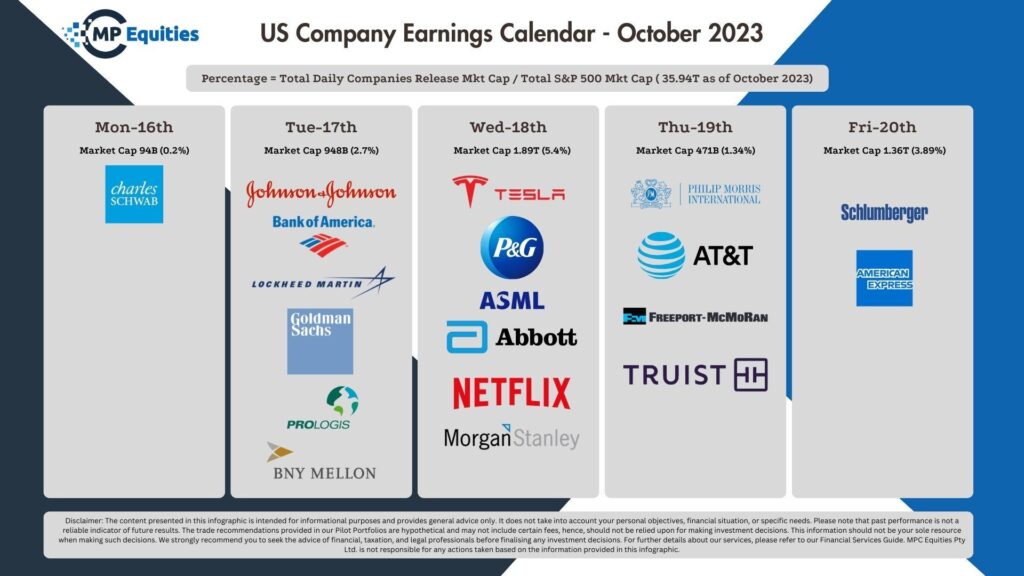

Calendar

Economic

US Quarterly Earnings