Skip to content

Skip to content

Last Night's Market Recap

Overnight – Big tech shrugs off geopolitics and rising yields to finish higher on earnings optimism

Equities rallied overnight as investors piled back into big tech, shrugging off an ongoing climb in Treasury yields as optimism of quarterly earnings expected this week.

Big tech, excluding Apple, were on the front foot, led by Microsoft and Alphabet as investors shrugged of rising Treasury yields. Apple cut the bulk of its losses to end flat after the stock was pressured by worries that sales of its iPhone 15 were lower in China in the earlier weeks after release, when compared to the iPhone 14, pointing to softer demand. Sales of iPhone 15 fell by a double-digit percentage from its predecessor amid stiff competition from Huawei’s Mate 60 Pro, Jefferies said in a note.

Charles Schwab reported mixed third-quarter results after revenue fell short of estimates, but the fall in deposits wasn’t as bad as feared. Schwab’s Q3 bank deposits fell to $284.4 billion from $304.4 billion in the previous quarter. Charles Schwab is down about 34% year to date, as the brokerage firm has suffered as clients moved into cash into high-yield products.

Pfizer was upgraded to Jefferies to buy from hold as the pharmaceutical giant’s plan to cut $3.5 billion costs is expected to bolster earnings. Its shares rose more than 3%. Pfizer cut its full-year guidance for earnings and revenue on Friday after warning of $5.5 billion in write downs in Q3 related to lower-than-expected sales of its COVID-19 vaccine and treatment. Covid vaccine related sales of about $1.6 billion made up less than 15% of Pfizer’s overall $12.73 billion revenue reported in the second quarter.

Crypto-related stocks were up sharply, underpinned by a more than 5% jump in bitcoin after a false report that Blackrock application for a spot Bitcoin exchange-traded fund, or ETF, had received approval from the SEC

S&P 500 - Heatmap

Commodities

Bonds

The Day Ahead

ASX SPI 7095 (+0.68%)

The ASX is likely to open higher on gains in the US, although a pullback in energy and gold prices may hold back the materials sector. RBA meeting minutes will be released which should give some context to the central banks thinking, while industrial production numbers globally will give some insight into economic activity over the coming days

The local market has been stuck in a 10% range this year, spending most of the time within a 6% range, holding the downside of 6900 which is remarkable given the sharp rise in interest rates globally. Highly cyclical sectors like consumer discretionary and industrials have been the best performers for the year, a common move during a hiking cycle, which turns nasty once talk of rate cuts begins.

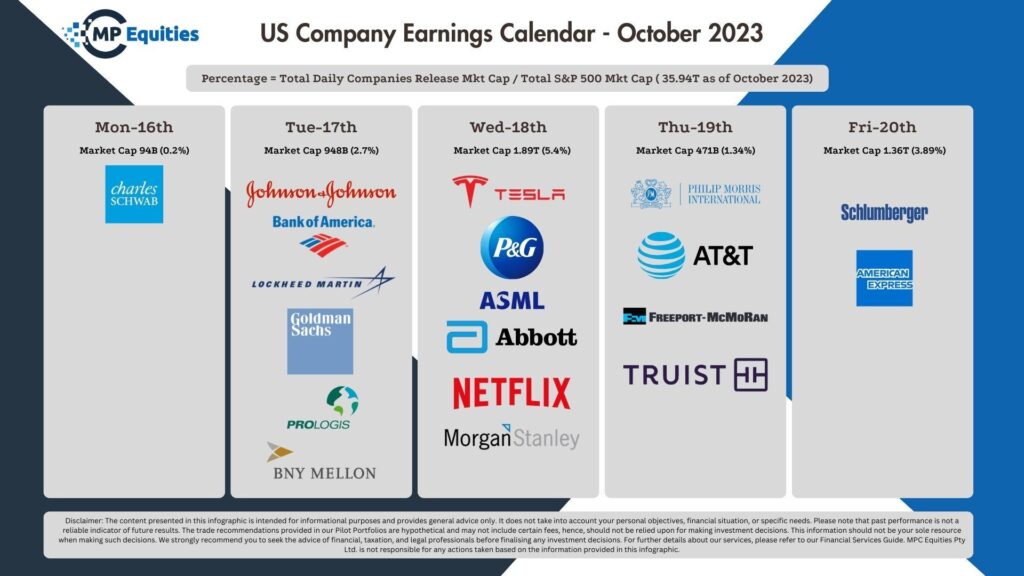

Sales and production results are scheduled for Challenger, Newcrest Mining, HUB24, Rio Tinto, St Barbara and Syrah Resources. Bapcor, Cochlear, IDP Education, SG Fleet Group and Telstra all host AGMs.

Calendar

Economic

US Quarterly Earnings