Skip to content

Skip to content

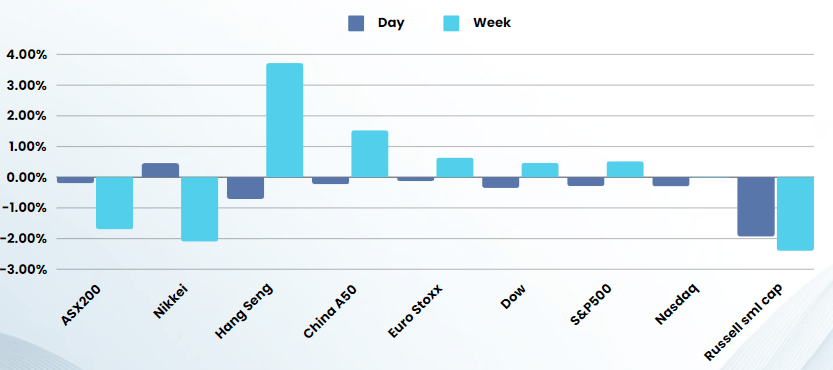

Last Night's Market Recap

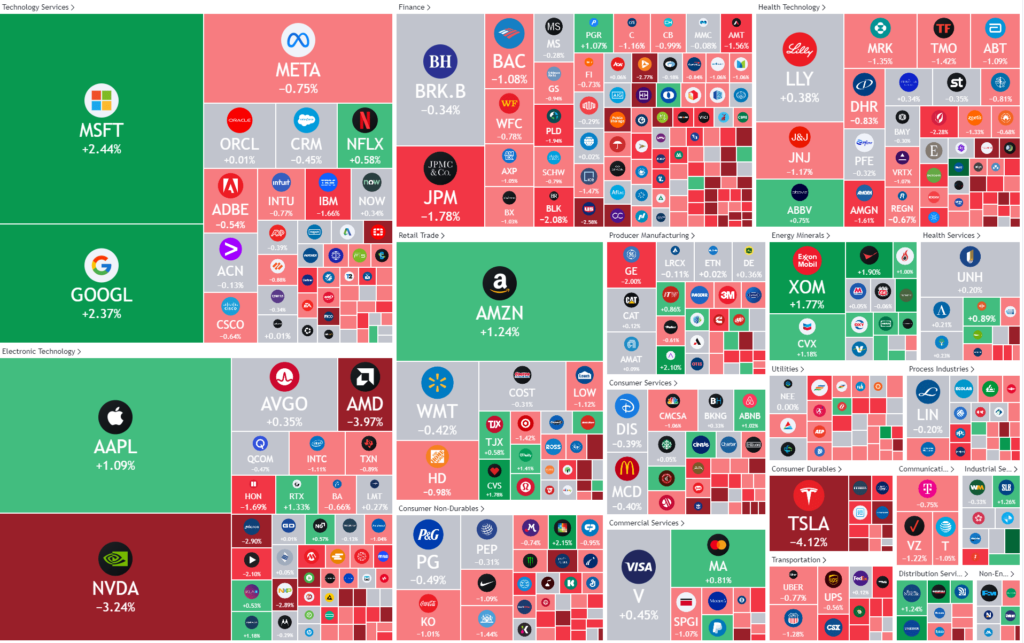

S&P 500 - Heatmap

Overnight – Persistent Inflation figures put the brakes on bull run

Equities sold off overnight as data showing inflation is running hotter-than-expected and signs that the consumer is pulling back weighed on investor sentiment.

Headline PPI inflation rose 0.6% month-on-month in February, data released earlier Thursday showed, taking the annualized rate to 1.6%, well above expectations for a 1.1% pace. The faster pace of wholesale inflation arrived on the heels of data showing signs of a weaker consumer after U.S. retail sales rose 0.6% month-on-month in February, below the 0.8% increase expected. The signs of slowing consumer spending comes even as the latest data showed Americans filing for unemployment claims stood at 209,000 for the week ended March 9, indicating the labor market remains under pressure. While many analysts are persisting with rate cut calls, the continual strength in the US economy and stubborn inflation corner the Fed into delaying cuts until there is a reversal.

The Fed kicks off its two-day meeting on Mar. 19 that is expected to result in an unchanged decision on interest rates, leaving many focused the bank’s updated economic and rate outlook that will accompany the decision.

Under Armour fell 10%, with investors expressing worries about the sports apparel retailer’s strategy after the announcement of the return its founder Kevin Plank as chief executive officer given the challenging economic backdrop. Electric vehicle maker Fisker slumped 51% after a WSJ report said the firm hired advisers for a potential bankruptcy filing. Robinhood stock soared 5% after the brokerage reported strong growth in assets under custody for the month of February, while Dollar General surged 5.6% after the discount retailer forecast upbeat 2024 sales, expecting steady demand from price-conscious shoppers.

We believe the current rate cut expectations are unrealistic and the US market is denial about the timing. If inflation persists for the next few months, we will be talking about rate hikes, not cuts

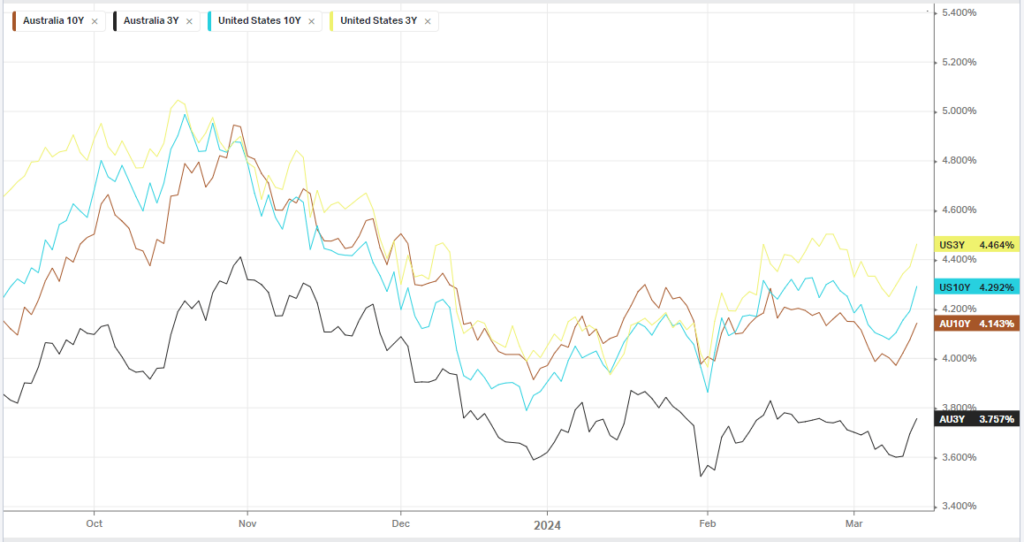

Bonds

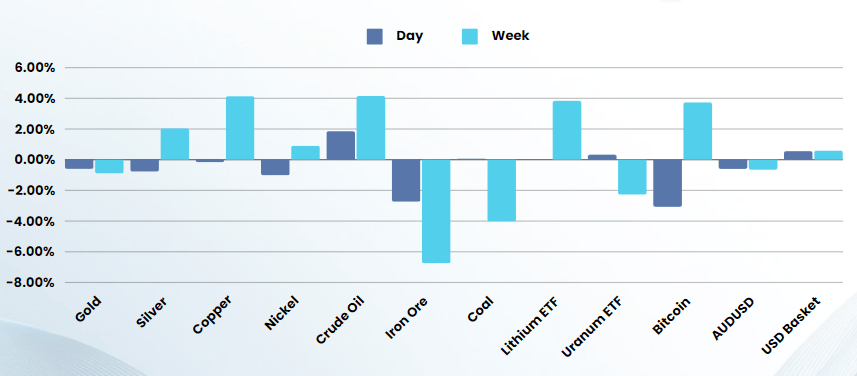

Commodities & FX

The Day Ahead

ASX SPI 7665 (-0.56%)

The ASX is in for a rough day as US inflation numbers have removes the heat from the rally. Materials and financials are the 2 largest sectors that contribute to our index and with the sharp fall in Iron ore prices and the weakness in global financial stocks, we are likely to outpace other global indices to the downside.

Company Specific:

- Lithium miners Liontown Resourcesand Sayona Mining both release results on Friday. CAR Group shares trade ex-dividend. In China, the one-year medium-term lending facility rate will be announced with new home prices data.

- Pilbara Minerals said it accepted a pre-auction offer for spodumene concentrate – a partly processed form of lithium – with the buyer paying the equivalent of $US1200 a tonne.