Skip to content

Skip to content

Last Night's Market Recap

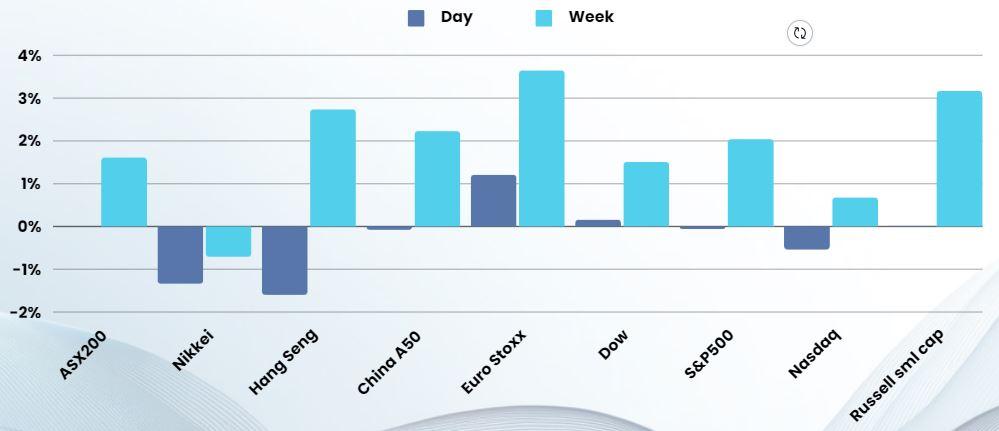

S&P 500 - Heatmap

Overnight – Disappointing Intel results end S&P500’s record run

Stocks fell away from record highs Friday, ending their five-day record run, though still ended the week in positive even as Intel’s slump left a dent in big tech.

The “core” personal consumption expenditures price index, which is the Fed’s preferred inflation guage and excludes volatile items like food and fuel, slowed to a 2.9% pace in December, from 3.2% a month earlier, below economists’ estimates of 3%. Further signs of slowing in inflation will likely be welcomed at the Fed as they prepared for the next policy meeting slated for Jan. 30-31. Consumer spending, which makes up the bulk of economic growth, surprised to the upside, rising 0.7%, well above estimates for a 0.4% rise, underpinning ongoing optimism the Fed’s measures to cut inflation are unlikely to push the economy into severe recession.

Europe’s equity index earlier closed up 1.1%, marking a 3% gain for the week, which was its biggest weekly percentage advance since the week starting Oct. 30. This was after the European Central Bank (ECB) signaled on Thursday that it could cut rates by April. While ECB chief Christine Lagarde said it was “premature” to discuss easing, money markets priced an almost 85% chance of a first quarter point rate cut in April.

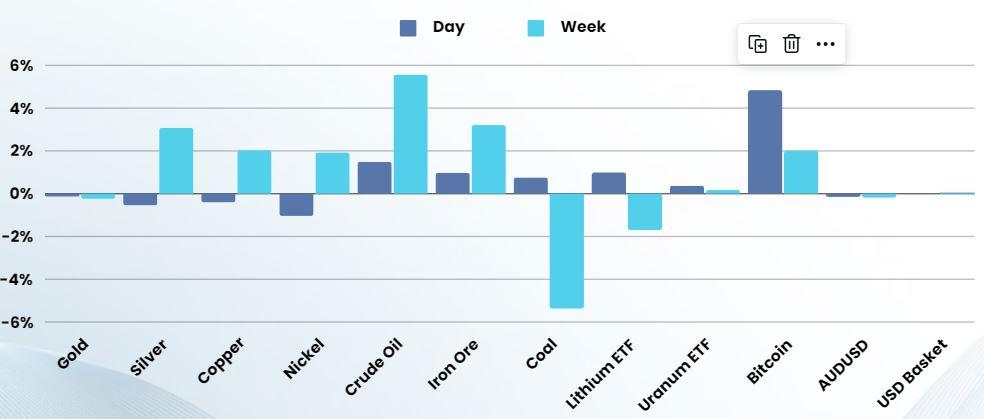

In commodities, oil prices settled higher as positive U.S. economic growth and signs of Chinese stimulus boosted demand sentiment, while Middle East supply concerns added support. U.S. crude settled up 0.84% at $78.01 a barrel, their highest settlement level since Nov. 29. Brent crude finished at $83.55 per barrel up 1.36% on the day for their highest closing level since Nov. 30. In precious metals, spot gold prices fell 0.06% to $2,018.58 an ounce as investors’ attention shifted to the Fed’s policy meeting next week as they waited for insights into the interest rate outlook.

US Earnings

- Intel’s disappointing first-quarter guidance sent shares of the chipmaker 12% lower and pressured tech stocks. Intel expressed significant confidence in quarter-on-quarter and year-on-year revenue and EPS growth returning for the remainder of 2024

- T-Mobile was marginally lower after the wireless carrier missed its profit target for the fourth quarter, even as it forecast monthly bill-paying phone subscriber growth for the year above estimates, banking on its wide 5G coverage and promotional offers to draw in consumers.

- American Express rose 7% after the credit card giant beat full-year profit expectations, even as it raised its loan loss provisions, bracing for a jump in potential loan defaults.

- Visa stock fell 1.7% after it offered up tepid second-quarter sales guidance, with the world’s largest payments processor forecasting an uptick in the “upper mid- to high single-digit” in net revenue during its current period — implying a slowdown from the 11% increase posted in the corresponding period in 2023.

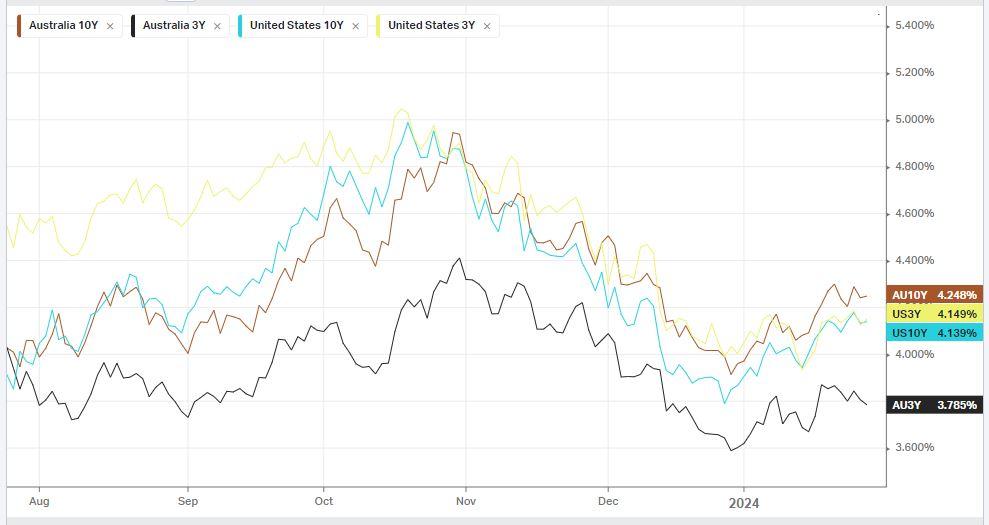

Bonds

Commodities & FX

The Day Ahead

ASX SPI 7553 (+0.18%)

The offshore markets may have fallen Friday night, however they ended up for the week, just off record highs. Tech was the laggard, which should affect our market too much. The rise in Iron ore prices should help the materials sector and rising oil prices the energy sector.

The focus this week will be firmly on US earnings and AU quarterly CPI

Market Calendar